Scanalyst

Silicon Valley Bank Collapses, Seized by Regulators

SCANALYZER

The Happening World

oops

,

california

,

silicon-valley-bank

,

bank-failure

eggspurt

6 April 2023 12:32

87

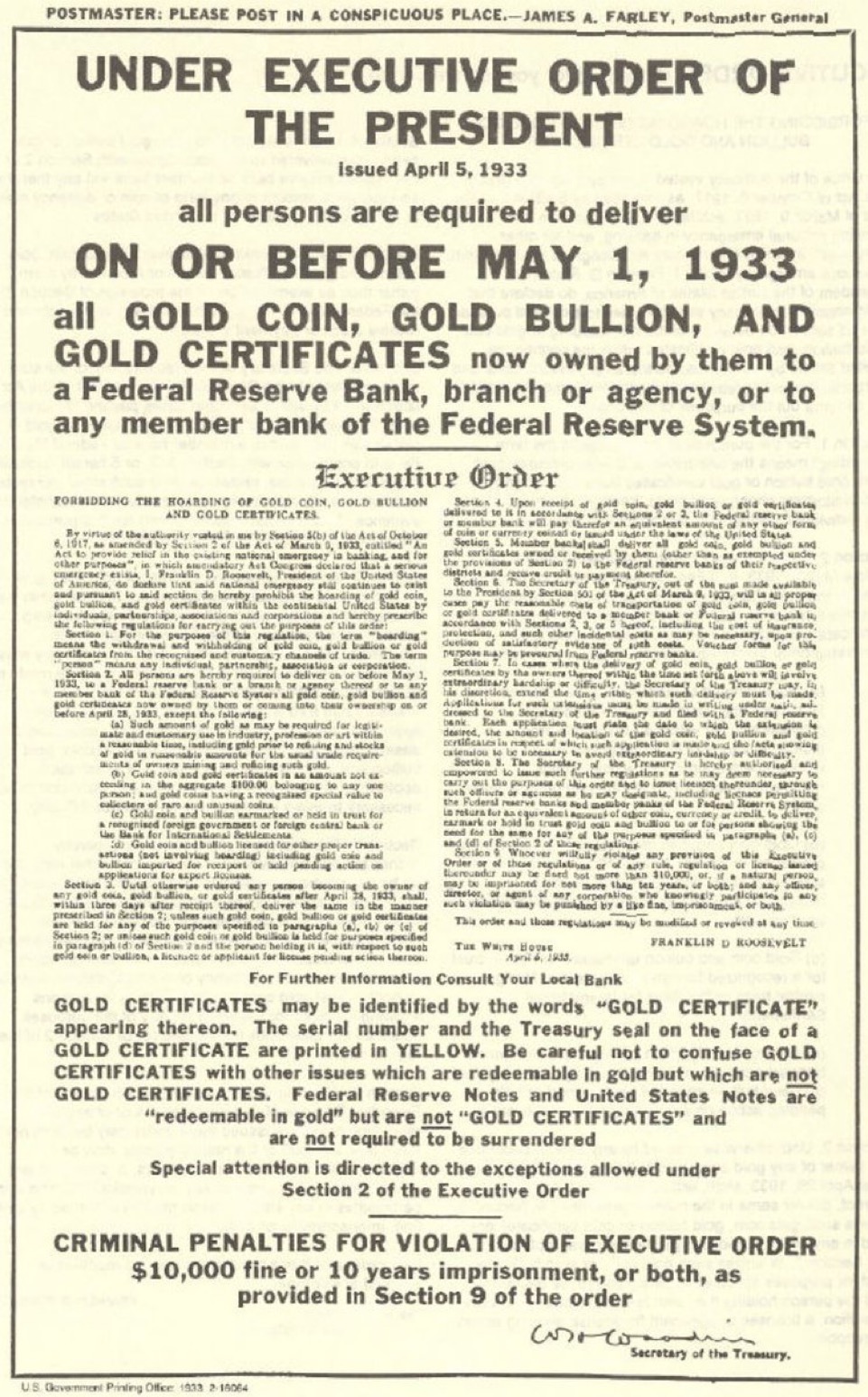

90 years ago, another type of seizure:

0F7279EF-D494-40F5-857B-74BCF69E71FB

961×1546 437 KB

4 Likes

A Tale of Adventure: Buying New Hearing Aids in the US

show post in topic