I’m not sure just how much prophetic ability you need when GPT4 can do a fairly decent analysis using Sept. 2021 data.

https://blog.matteskridge.com/business/gpt4-and-silicon-valley-bank/2023/03/19/

There is some clever hans prompting, but still…

I’m not sure just how much prophetic ability you need when GPT4 can do a fairly decent analysis using Sept. 2021 data.

https://blog.matteskridge.com/business/gpt4-and-silicon-valley-bank/2023/03/19/

There is some clever hans prompting, but still…

Oh, good grief…

Reminded me of a good blog post I recently read on playing games with the books.

Swissinfo.ch reports, based upon a 2023-04-02 article in Zürich’s SonntagsZeitung:

The megabank created by the UBS takeover of Credit Suisse is poised to reduce its global workforce by 20-30% – between around 25,000 and 36,000 positions – according to the SonntagsZeitung newspaper, citing an unnamed senior UBS manager.

This is far more than the 9,000 jobs Credit Suisse had planned to cut in its restructuring plan before the Swiss authorities forced UBS to buy out its imploding rival on March 19.

In Switzerland alone, up to 11,000 jobs would be affected….

Before the takeover, UBS employed just over 72,000 people worldwide, compared with more than 50,000 at Credit Suisse.

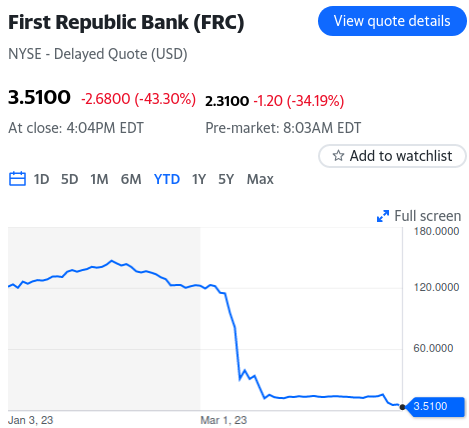

Well, it’s Commie Christmas, 2023-05-01, and about time for another pillar of the tottering funny money capitalist edifice to fall, so here we go again. At the start of the 2023 bank failure season, along with the collapse of Silicon Valley Bank and Credit Suisse, another “bank of concern” mentioned as being at risk was First Republic Bank, with headquarters in San Francisco, California and 93 branches, mostly in the People’s Republics of California, New York, Massachusetts, and the exile colony of Florida. The bank specialised in financial services for “high net worth individuals”, and became especially known for financing jumbo mortgages at low rates for players in the bubble residential real estate markets of California, New York, and Florida, including “interest only” loans where the borrower paid off none of the principal over the term of the mortgage. It was also a player in the once-hot commercial real estate markets in those locations, which are now facing a disastrous solvency crisis as tenants downsize, consolidate, and adapt to the work-from-home trend that has outlived the pandemic.

First Republic stock (FRC) has been on a vertiginous slide since early March 2023, with shares that traded as high as US$ 171 in the last year falling to less than US$ 3 in the last few days.

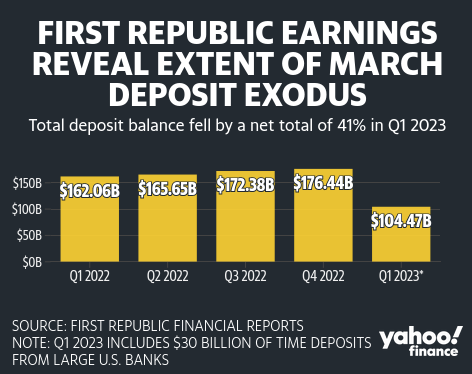

The most recent downward leg was triggered by their first quarter 2023 financial report, which showed them bleeding out deposits, losing 41% in just this one quarter.

It’s like the quote from Hemingway’s The Sun Also Rises, “How did you go bankrupt?" Two ways. Gradually, then suddenly.” As of the end of last week, First Republic was clearly in the “suddenly” phase.

After furious negotiations, arm-twisting, and brinksmanship over the week-end, as Commie Christmas dawned, something ironically named the California Department of Financial Protection and Innovation announced “California Financial Regulator Takes Possession of First Republic Bank”.

The California Department of Financial Protection and Innovation (DFPI) announced today that regulators have taken possession of First Republic Bank.

The DFPI appointed the Federal Deposit Insurance Corporation (FDIC) as receiver of First Republic Bank. The FDIC has accepted a bid from JPMorgan Chase Bank, National Association, Columbus, Ohio, to assume all deposits, including all uninsured deposits, and substantially all assets of First Republic Bank.

The DFPI took action pursuant to California Financial Code section 592, subdivisions (b) and (c), specifically “conducting its business in an unsafe or unsound manner” and being in a “condition that … is unsafe or unsound” to transact banking business.

The U.S. Federal Deposit Insurance Corporation (FDIC) said:

First Republic Bank, San Francisco, California, was closed today by the California Department of Financial Protection and Innovation, which appointed the Federal Deposit Insurance Corporation (FDIC) as receiver. To protect depositors, the FDIC is entering into a purchase and assumption agreement with JPMorgan Chase Bank, National Association, Columbus, Ohio, to assume all of the deposits and substantially all of the assets of First Republic Bank.

JPMorgan Chase Bank, National Association submitted a bid for all of First Republic Bank’s deposits. As part of the transaction, First Republic Bank’s 84 offices in eight states will reopen as branches of JPMorgan Chase Bank, National Association, today during normal business hours. All depositors of First Republic Bank will become depositors of JPMorgan Chase Bank, National Association, and will have full access to all of their deposits.

Deposits will continue to be insured by the FDIC, and customers do not need to change their banking relationship in order to retain their deposit insurance coverage up to applicable limits.

The FDIC went on to note:

The FDIC estimates that the cost to the Deposit Insurance Fund will be about $13 billion. This is an estimate and the final cost will be determined when the FDIC terminates the receivership.

As of 2022-12-31, the FDIC’s Deposit Insurance Fund had a balance of US$ 128.2 billion. The hit to the fund for Silicon Valley Bank was estimated at US$ 20 billion, so together with First Republic, these two collapses have consumed almost 30% of the insurance fund. The First Republic collapse is the second-largest bank failure in U.S. history (in nominal dollar terms), after Washington Mutual in 2008.

ZeroHedge has much more about the details of the deal with JPMorgan and how, as usual, the taxpayers will end up on the hook for First Republic’s toxic loans, while Morgan will harvest the deposits and well-heeled customers who are too stupid to get out of the U.S. and its crooked financial system while they still can.

While JPMorgan CEO Jamie Dimon said on an investor call on 2023-05-01, “The system is very, very sound.”, Yahoo Finance reports:

The US government decided to make a critical exception in handing First Republic to JPMorgan. There is an existing rule preventing any bank from making an acquisition providing it with more than 10% of all US deposits, and JPMorgan is already above that cap. Regulators waived those deposit concentration restrictions and blessed the deal anyway.

Sounds very. very much like a “system” to me!

Merry Commie Christmas, comrades!

So the FDIC will be liquidating its own assets in order to pay for these problems. But liquidating assets will drive the price of those assets down (supply & demand) – potentially triggering “mark to market” issues for other investors. This is how “gradually” can accelerate into “suddenly”.

I wonder what the FDIC holds as assets it can sell? Maybe US Treasury bonds? Those are guaranteed safe!

But what is an investor to do? Liquidate his assets in the US and move them to ever-reliable … Switzerland? No problems there!

I wonder where the 50 billion loan to JPMorgan will come from? Seems like the FDIC will be left with 30 to 40 billion in liquid funds. Not to mention the FDIC estimated $13 billion. Hmmm, estimated. Just recently the big insider banks deposited 30 billion to prop up this bank and obviously that estimate was way off and was only good for about 3 weeks. Certainly that 30 billion wasn’t covered by FDIC insurance and yet they will be made whole. I don’t understand banks, but it seems like the liabilities are 104.47 billion. The FDIC is coming up with at least 63 billion. Reducing the liabilities to 41.47 billion. The assets include 30 billion in securities and 170 billion in bonds. So 200 billion in assets cannot cover 41.47 billion in liabilities? Give me a break. JPMorgan got the assets at 20 cents on the dollar. My guess is it will turn out to be 10 cents on the dollar after the real liability of the FDIC turns out to be higher.

PS Odds are the loan JPMorgan received has similar terms as the COVID PPP loans. Loans that don’t have to be paid back,

I think a new epithet is required to describe our financial system. We are so far beyond the "smoke and mirrors’ phase, a novel sobriquet is screaming to come into existence. I’m coming up blank (I suppose that, itself, has significance since as far as US finance is concerned I am a mere NPC).

“Fiat Fantasy”

by GPT-4, as prompted by John Walker.

Prompt:

Please write a humorous rhyming poem in the style of Ogden Nash titled “Fiat Fantasy” about the modern monetary and banking system, with inflation, bail-outs, and overnight bank failures.

Reply:

In the land of the dollar and yen,

Where money is made by invisible men,

A tale unfolds of a system bizarre,

A financial realm that is quite a la carte.

In the days of yore, with gold they did barter,

But now they just print, in a manner much smarter.

From thin air, it appears, this currency green,

A dreamy delusion, a capitalist’s dream.

The banks, they do lend, and the people do borrow,

As they dance to the tune of the Wall Street tango.

With interest rates high, and debts even higher,

The money, it flows, like the Thames or the Tiber.

Inflation’s a word that they’d rather not mention,

It’s the demon that lurks in each banker’s intention.

As prices do rise, and the people do fret,

Their savings, they wane, like the sun as it sets.

The bail-outs arrive, like a knight in gold armor,

But for every dollar, there’s a gory new drama.

The banks, they do fail, as they’ve done overnight,

A fickle existence, a fiscal delight.

In the end, we ponder the fate of this scheme,

Is it real, or a fantasy woven from dreams?

As the dollars and yens and the euros do tumble,

In the game of finance, we all tend to stumble.

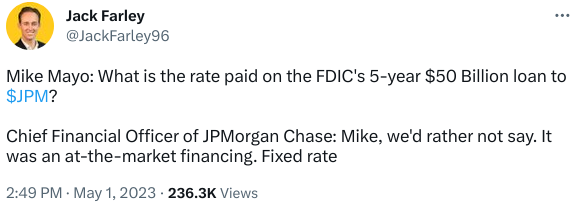

The US$ 13 billion was described in the FDIC press release as “(about) the cost to the Deposit Insurance Fund”. By this, I presume, they mean the ultimate draw-down of the fund to pay off insured depositors. Since the US$ 50 billion loan (which is not mentioned in the press release) is a loan, and JPMorgan is certainly good for the money (right, right?) that is not considered a loss to the fund, since they can carry the IOU on their books as an asset until it’s paid off. What are the terms of this loan, you ask?

Don’t ask. A little bird tells me it’s probably a lot less than the big bank prime rate that they charge their most creditworthy corporate customers, which is presently 8%, up from 3.5% a year ago.

This deal is very complicated, with lots of moving parts. As to the US$ 30 billion deposited in First Republic (FRC) by the big banks in the first, doomed, rescue of FRC, US$ 25 billion will be repaid to them (presumably from the US$ 50 billion FDIC loan) and the US$ 5 billion loaned by JPMorgan will be written off.

Another key part of the deal is the “loss share agreements”. In the FRC loans taken over by JPMorgan, the FDIC will provide an 80% backstop loss coverage for 7 years for residential mortgages and 5 years for commercial loans, including real estate. To the extent these default, the FDIC (a.k.a. bagholders taxpayers) will be on the hook for 80% of the losses. Further JPMorgan gets to reduce the risk weighting of these covered loans to 25% in computation of meeting their capital requirement, keeping that sweet leverage music playing a bit longer.

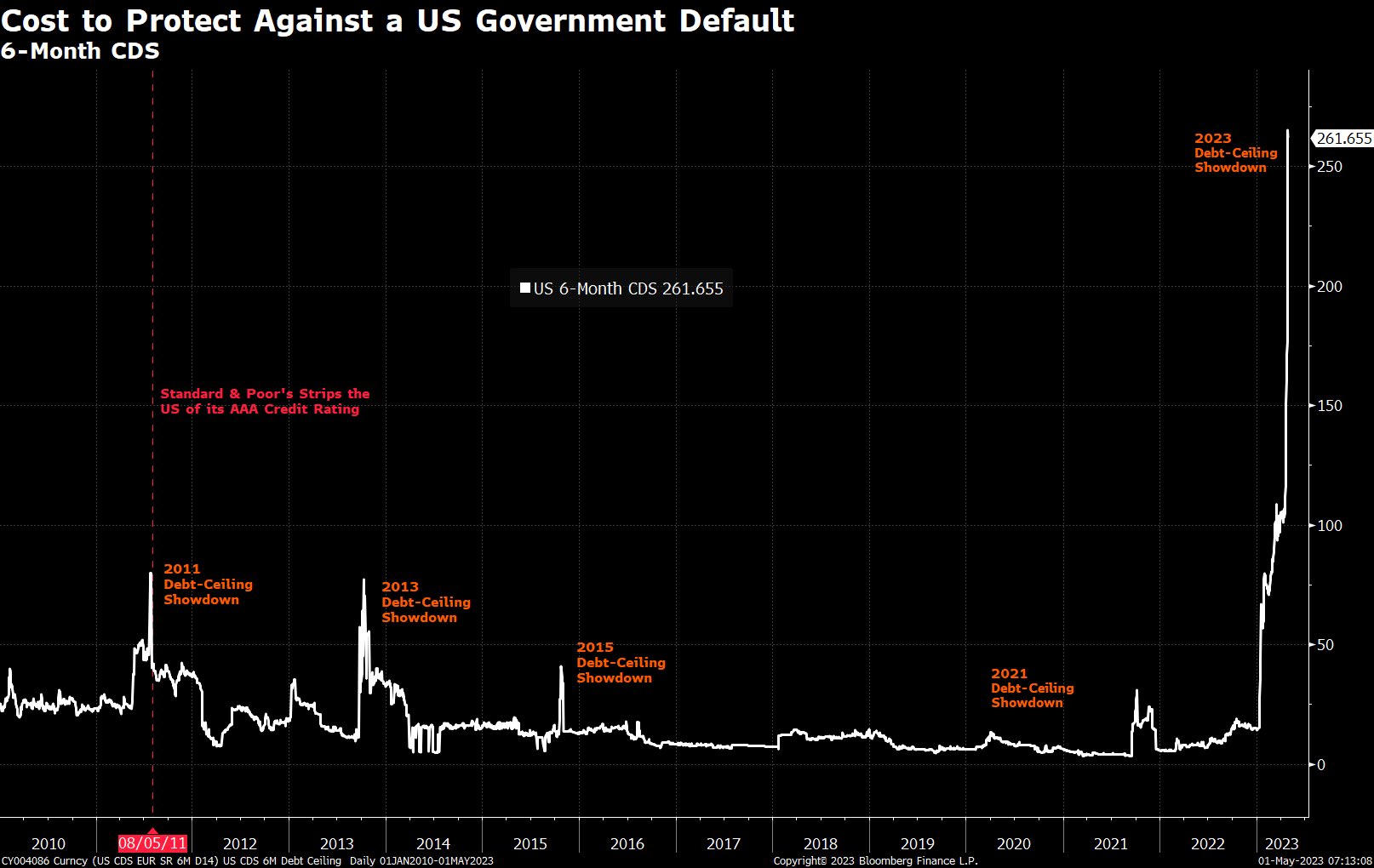

What is the source of that graph of “Cost to Protect Against a US Government Default”?

You can see it in the bottom: Bloomberg.

Tuesday, November 5, 2024 is the election day. As long as the music keeps playing until then… All is good. Right?

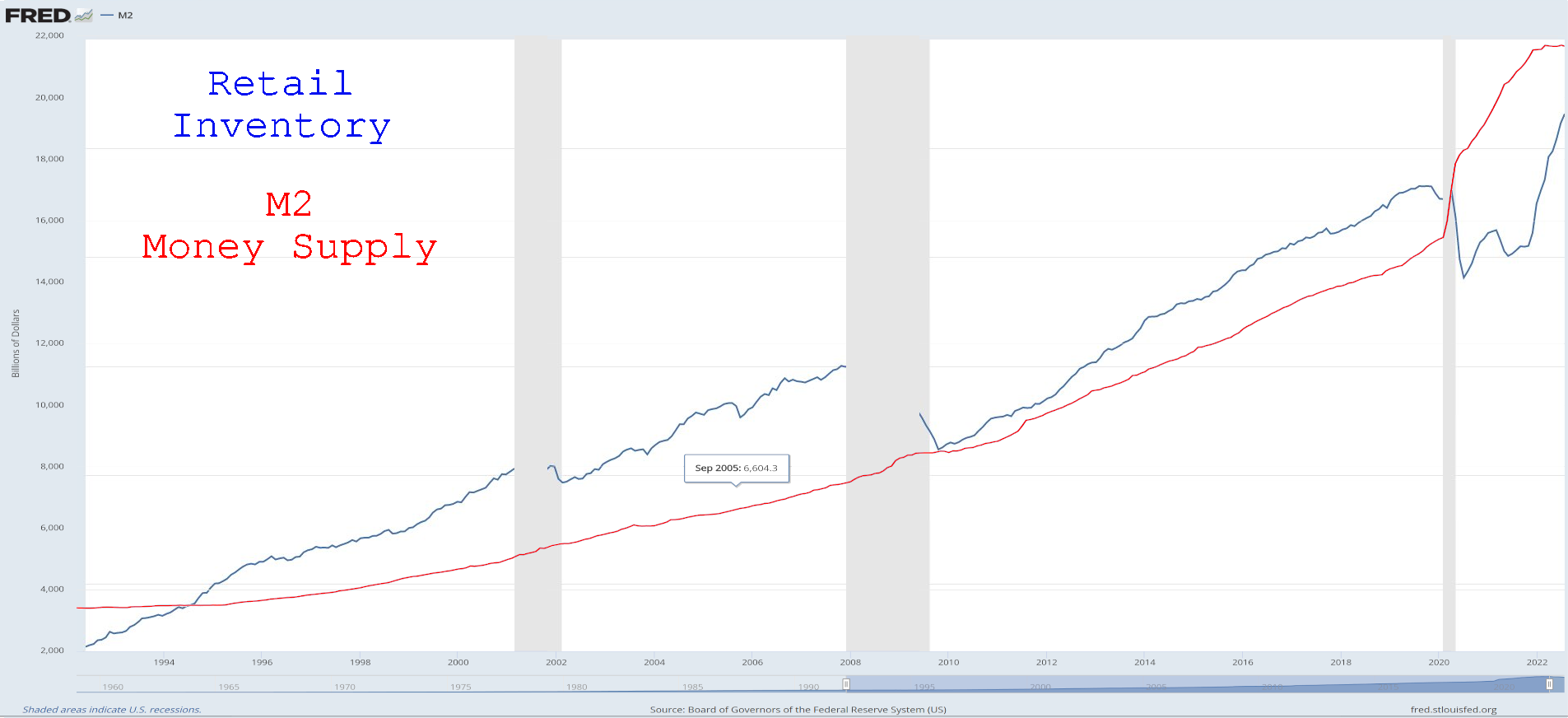

Interesting that retail inventory is going up despite all that money being injected into the system. Who is sitting on all that money?

Balaji posted his presentation yesterday, including “proof of work” regarding the pledge to pay $1M.

The pitch is “perfect storm” + “slowly, then suddenly”

https://nitter.net/balajis/status/1653449321185169409

He pegs the probability of the global fiat crisis being months away at 10%.