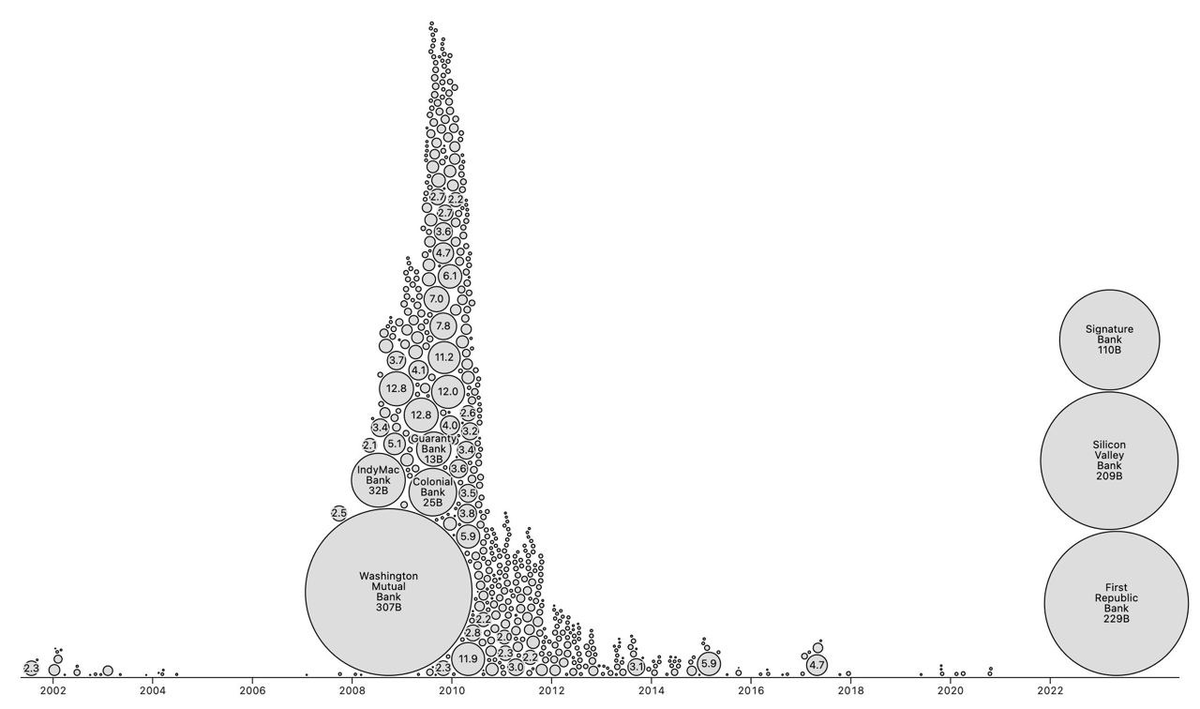

The regional banks then proceeded to go blooie!, led by PacWest Bancorp ($PACW), whose stock had traded above 26 in early March before taking two vertical hits on the Silicon Valley Bank and First Republic collapses to close at US$ 6.42 on 2023-05-03. But Powell spake after the market close, whereupon $PACW collapsed another 60% almost instantaneously to below 2. It has since recovered to around 4 in pre-market trading, down a mere 36% since yesterday’s close. We’ll see what happens when the market opens today. PacWest has its headquarters in Beverly Hills, California and paid its executive chairman US$ 4.27 million last year for his financial wisdom and foresight.

PacWest has US$ 48 billion in assets and US$ 28 billion in deposits, which are probably evaporating like the morning dew on Mercury.

“Sound and resilient”.

Update (2023-05-04 15:45 UTC): Trading in PacWest has been halted on and off, with the last quote at US$ 3.32/share, down 49.7% from yesterday’s (May 3) close. Western Alliance Bancorporation ($WAL) has joined the party, down 33.9% on the day so far. Western Alliance is headquartered in Phoenix, Arizona, and paid its CEO US$ 4.51 million last year. Trading in its stock has also been halted sporadically during the day.

Aren’t these the same guys who repeatedly told us - in actual recent memory (and not yet amenable to the memory hole) - that inflation was “transient”?

It’s a matter of time scale… perhaps Janet and Jerome are thinking of transitory on the timeline of the heat death of the solar system? In which case they’re not wrong

Leaving cheap shots aside, the recent Vovan and Lexus pranks with Jerome and Fifi Lagarde uncovered the absence of higher order thinking in the top echelon.

Frankly, I do not understand why failure of 3 banks out of ~4k banks comprising the bank system is an indication of system failure. In my view, the fact that a few banks could take all the rope they needed to hang themselves is an indication of certain freedom allowed by the system. This freedom may lead to innovation or to failures. The system then cleaned up the failures – none of the shareholders of these banks were bailed out to my knowledge. Is not it the capitalism at its best?

If PACW held long-term assets against short-term obligations, we should let it burn as well, at least, as far as shareholders and possibly bondholders are concerned. I do not see how this undermines the system.

As far as 0.25% rate hike, the FED could have saved it for the meeting in June. Resuming hikes after a brief pause would only reinforce the idea that the FED is serious about the inflation.

Financial speculators seem to spend a lot of time focused on the Fed. And yet the Fed is not the source of the problem. The fundamental cause of all the problems is FedGov foolishly spending more money than it takes in year after year. The Fed is guilty of facilitating that FedGov stupidity – but if the FedGov started to behave responsibly and spend less than its income, the Fed would have a much simpler task.

It is a good thing that FedGov’s over-spending is under the control of democratically-elected Representatives of the people. Those courageous men & women & transgenders will put a stop to the excessive spending – for sure. Democracy is wonderful!

If the 3 or 4 bank failures was the end of it, it wouldn’t be a system failure. My concern is that this is just the beginning. A factional bank reserve system cannot handle a situation where everyone wants their deposits.

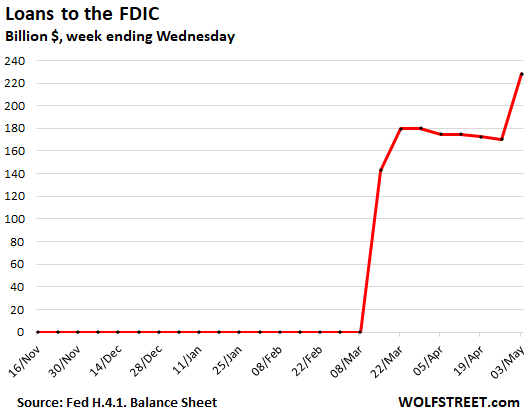

It is not just deposits over the insured limit will be pulled or that people may get concerned that the FDIC cannot really back deposits with only 120 billion in funds, people will also figure out that getting 0.1% interest on you savings is a really bad deal and move to money market accounts etc. The systemically important banks seem to be counting on TINA or maybe the powers that be are forcing TINA. You will deposit your money at these five banks and they will not pay you for it.

In a debt based system, the “real” (if you can call the US economy real) depends on loans to function. If banks decide not to loan, there can be a death spiral.

I agree banks should be allowed to fail and capitalism requires that poor businesses fail. However, the system has been corrupted and therefore doesn’t follow capitalistic principles. Low interest loans to the government and consumer loans are not great assets. My thought is that once an economy becomes overly dependent on discretionary consumption (Uber eats anyone?) and what is being consumed is not made in the same jurisdiction, you have a huge problem.

When I look at money supply growth and the economic equation that relates money supply to GDP based on velocity, there are big swings in velocity. Velocity is not measured. It is calculated. Is there any way to know the formula is right when you don’t measure the variables? I don’t know how this basic formula doesn’t get questioned. We increased the money supply 8% over multiple years and GDP grows at a much slower rate and it is assumed velocity dropped. Wouldn’t electronic transfers increase the velocity when compared to paper checks. I would assume that the relationship between money supply and GDP is flawed. Productive growth should drive money supply, but the big brains say that money supply drives productive growth. I would worry that all that money supply went to fund non-productive things and given the money supply comes from the commercial banks, I worry that there is a whole bunch of bad assets regardless of whether they are marked to market or held to maturity. Any bond that pays near zero percent in a 2% inflationary environment is not a good investment. There is no way in free market capitalism that bond interest rates are zero or negative. That can only be done by manipulation of the price of money. I think velocity dropped because those closest to the printer get the money. What do they do with the money? They buy paper assets (stocks, bonds) or invest in start ups. Driving yields down and PE ratios up for paper assets and having too much money for productive start ups they fund a whole host of companies that never make money. Very little productive investment that drives GDP. It may drive consumption based on the so called wealth effect of the stock market bubble, but when the bubble runs out of new air the party is over. Thus, the markets infatuation with what the FED says because the market isn’t based on a real economy. Crazy things happen when the paper asset price is based on creating a bunch of money. Like a market rally into a recession.

By the way: The depositors that exceeded the FDIC limit did get bailed out. So thus far, no bank has been allowed to fail and follow the normal failure process.