Following Biden’s speech, First Republic Bank dropped to 21.83, down 73.30% from Friday’s close. Other banks are also selling off.

Gold is up US$50.40/troyounce to 1917.60, +2.7%, silver up 6.9% to 21.92, and Bitcoin up 16.39% to 23,923.10 US$/BTC.

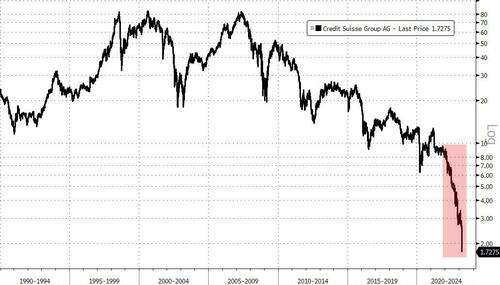

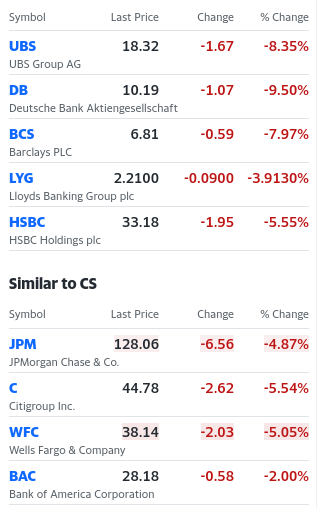

In Europe, Credit Suisse dropped 15%, hitting a new record low, while its five-year credit default swaps jumped to 448 basis points, also a new record. And it isn’t just Credit Suisse—here are other European banks’ CDS.

Banking has always faced the problem of borrowing short to lend long. The only factor which makes this work is “trust”. If investors start to worry about trusting banks, how much longer until they start to worry about trusting Big Government?

It seems though that her boss overruled her - here is Joe Biden on Monday morning (US time) - video + transcript (video source & WH transcript source)

Treasury Secretary Yellen and a team of banking regulators have taken action — immediate action. And here are the highlights:

First, all customers who had deposits in these banks can rest assured — I want to — rest assured they’ll be protected and they’ll have access to their money as of today. That includes small businesses across the country that banked there and need to make payroll, pay their bills, and stay open for business.

No losses will be — and I want — this is an important point — no losses will be borne by the taxpayers. Let me repeat that: No losses will be borne by the taxpayers. Instead, the money will come from the fees that banks pay into the Deposit Insurance Fund.

[…]

And what will banks do with those fees? Surely they won’t pass them on to the taxpayers… right, Joe? … Not a good look.

Since the Fed is in a giving mood, Bill Ackman is piling on…

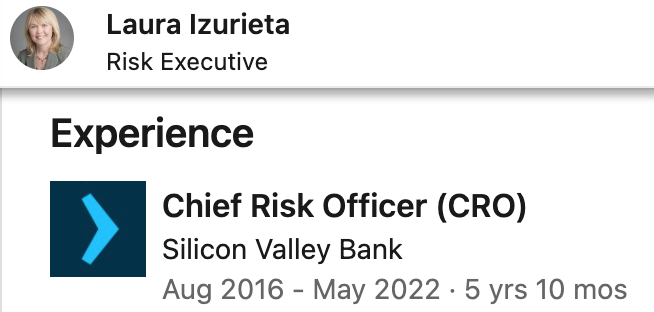

The former SVB Chief Risk Officer is still looking for a job if anyone’s interested?

Financial Services and Enterprise Risk Management expert skilled at creating strategies that imbed well-managed practices in the business delivering true business value. Effectively manage all aspects of risk by partnering with business executives who are driving an aggressive innovation agenda. Senior Executive with 20 years of achievements in operations, risk management, large program delivery and culture change. Drive innovation, enhance customer experience and bottom-line performance by combining business expertise with tactical execution. Natural leader with strong team-building skills and ability to inspire, empower, and motivate. Focused on team performance and development with a hands-on approach to creating and managing a successful organization.

Adam Tooze has a good explainer regarding the SIVB unpleasantness up to and including Saturday March 11. Very thorough with many links to insights from other commentators.

In Monday’s lawsuit, shareholders led by Chandra Vanipenta said Santa Clara, California-based SVB failed to disclose how rising interest rates would undermine its business model, and leave it worse off than banks with different client bases.

The lawsuit seeks unspecified damages for SVB investors between June 16, 2021 and March 10, 2023.

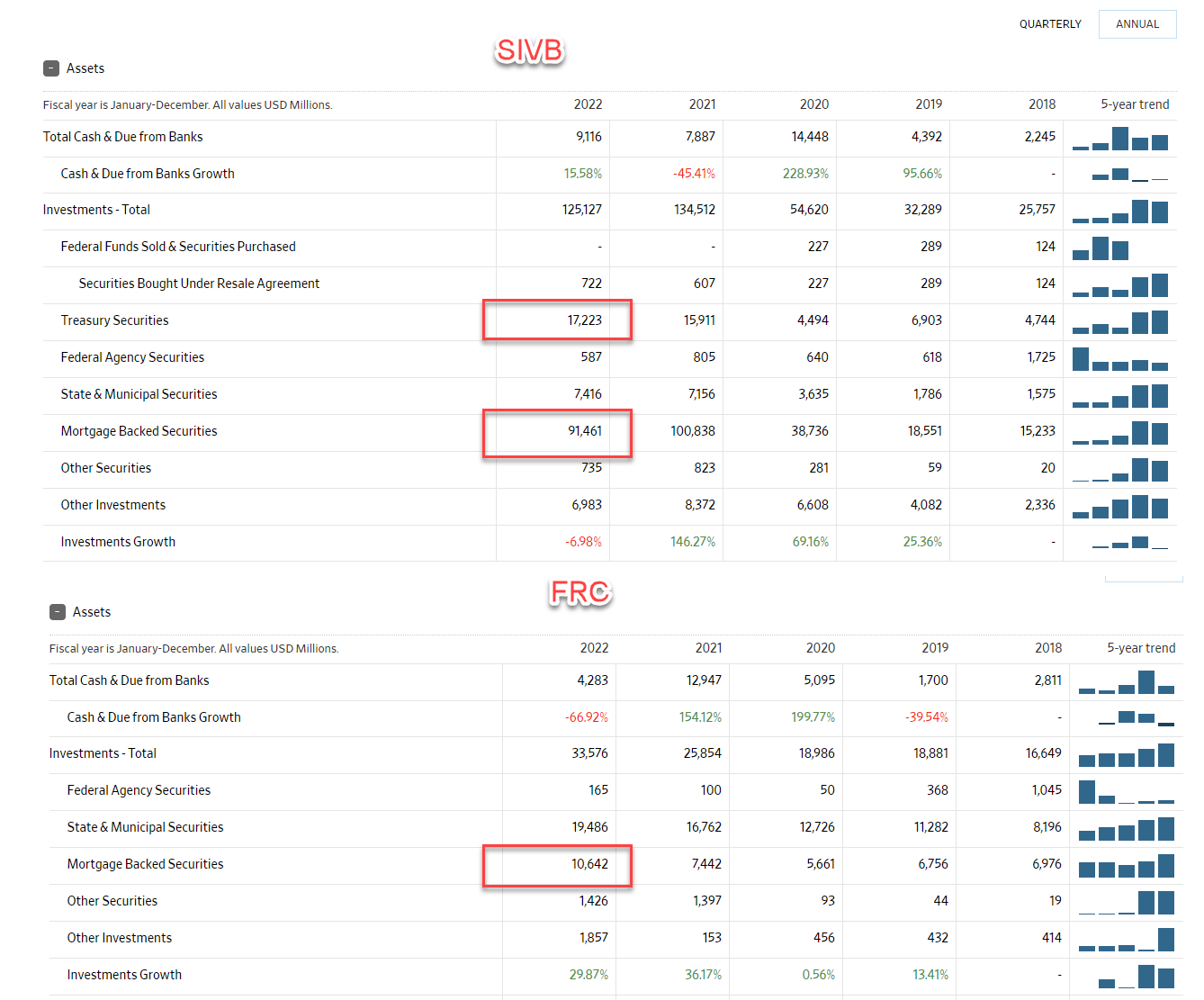

One key revision [of the 2018 bipartisan bill] was the Fed’s decision to exempt banks with $100-$250 billion in assets from maintaining a standardized “liquidity coverage ratio” as long as they kept their short-term wholesale funding levels below a certain amount. The ratio is designed to show whether a lender has enough high-quality liquid assets to survive a crisis. A lack of liquidity turned out to be a major problem for Silicon Valley Bank as deposits left the bank and the value of its assets declined as interest rates rose.

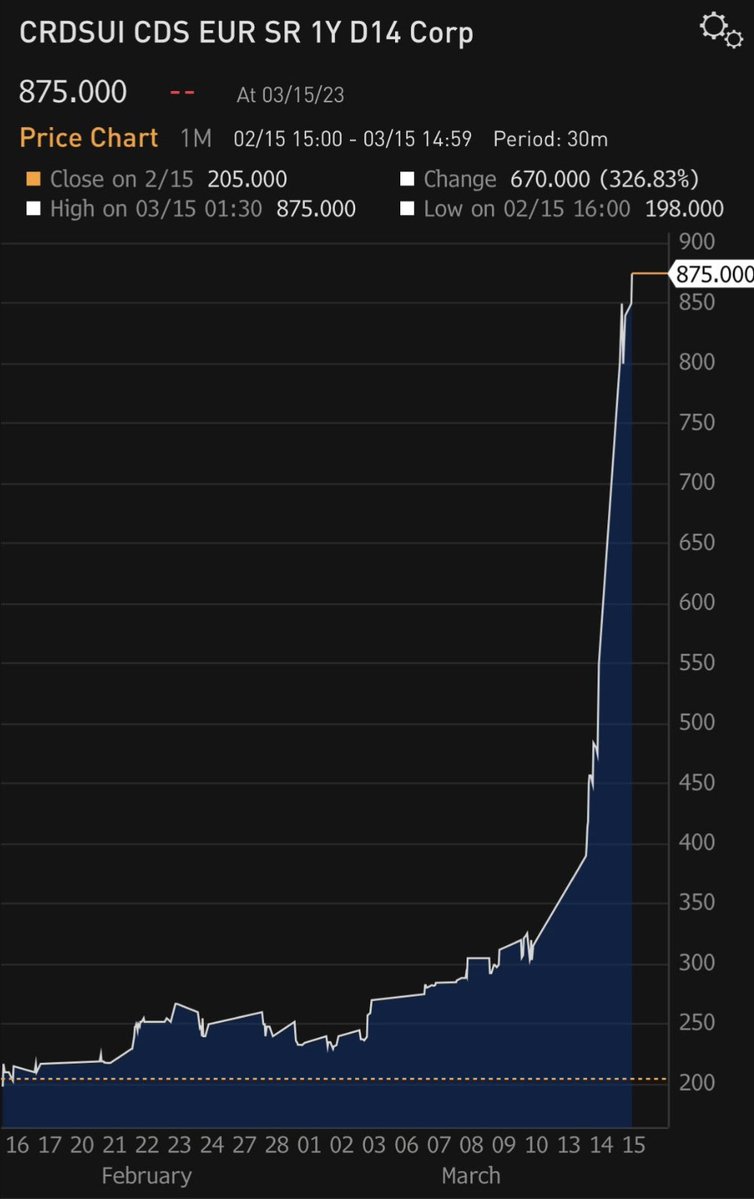

Remember those halcyon days of yore six hours ago when I wrote about Credit Suisse one year credit default swaps hitting an all-time record high of 875 basis points. Well, here’s that chart updated as of the U.S. market close on 2023-03-15.

Two thousand seven hundred and twenty-eight—875 barely looks like a blip on this chart. The general rule of thumb is that 1000 is the “default danger zone” for a debtor.

Credit Suisse announces it plans to borrow up to CHF 50 billion from the Swiss National Bank to “pre-emptively strengthen liquidity”.

The press release says the loan is “fully collateralized by high quality assets”, which essentially means Credit Suisse pledged just about all of its remaining assets as collateral for the loan. The big question is whether this will be sufficient to stop the hæmorrhage in deposits. In Switzerland, deposit insurance covers only the first CHF 100,000 in an institution.

Here we go again. One day after the “rescues” of First Republic Bank, which specialises in real estate loans to high net worth individuals buying properties in California and New York and Credit Suisse by the Swiss National Bank as of 17:53 UTC today, 2023-03-17, First Republic Bank (FRC) is down 25% on the day, Credit Suisse (CS) is trading at US$ 1.965/share, down 9%. In the race to safety, gold is up US$ 53.8/troy ounce (2.8%) and Bitcoin is up 7.3% to US$ 26,497/BTC.

When words are the appeal of last resort in dispute processing, words become swords and there is no distinction between the initiation of force and the initiation of discourse.

Honor is moral territory, which is why “honor culture” has a negative connotation nowadays.

I mean how can there be moral hazard when there is no morality?

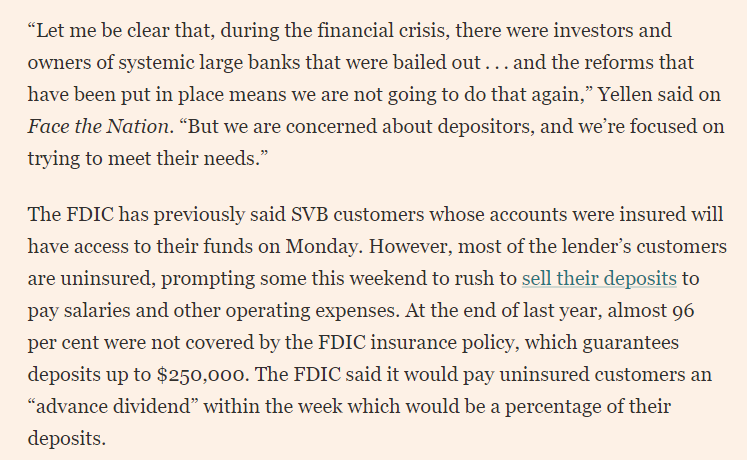

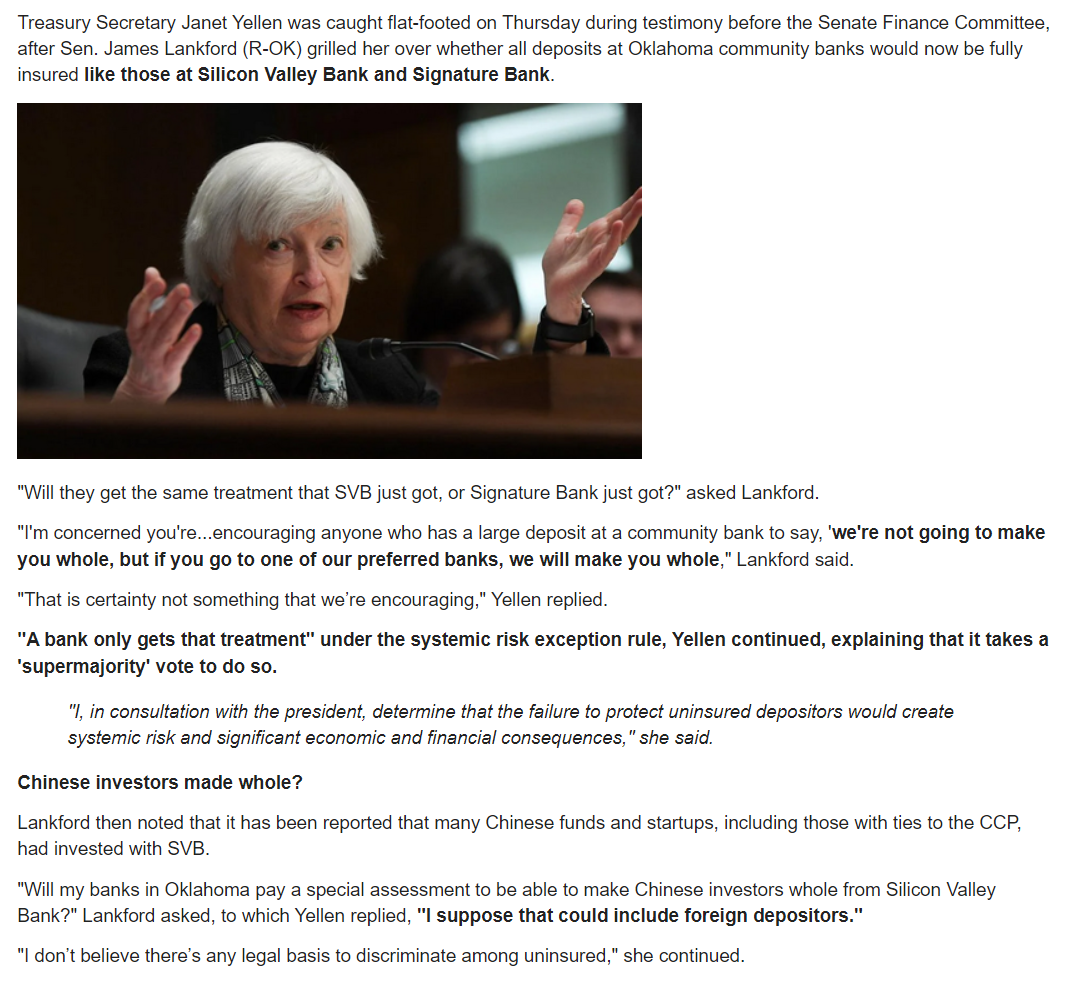

This is the “Treasury Secretary” of the United States, testifying before the U.S. Senate finance committee that while uninsured depositors of “systemically important” banks will be “made whole”, depositors in other small banks cannot expect to be compensated for deposits above the US$ 250,000 insurance level. It is estimated that around 50% of deposits in community and regional banks exceed this level. What, other than stupidity, is going to keep those holding these deposits from moving them to the big “systemically important” banks starting at the opening of business on Monday, 2023-03-20? What happens then?

Here is Yellen’s entire testimony, almost three hours. You can scroll to almost any point for further examples of Yellen’s cluelessness. But then, when you are in charge of a “Treasury” whose “treasure” amounts to a US$ 31 trillion smoking hole in the ground, how smart to you have to be?

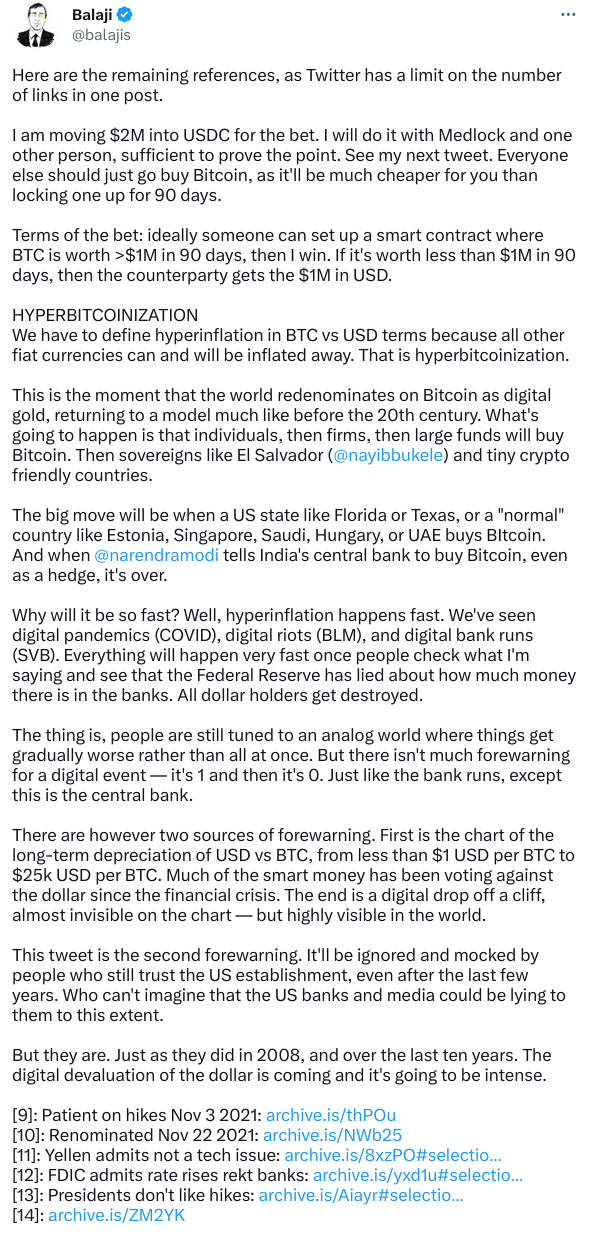

Balaji Srinivasan, author of The Network State, has bet US$ 1 million against 1 Bitcoin that the US$ will go into hyperinflation within 90 days resulting in the US$ price of Bitcoin rising to US$ 1 million/BTC.

Flaw in this is obvious. When/if 1 Bitcoin rapidly rises to be tradable for $1,000,000 (i.e. $1 drops in value to almost nothing), the chances of there still being reliable electric & internet availability drops to near-zero, and Bitcoin will be effectively untradable. By that stage, anyone with $1,000,000 would rather use it to buy a real can of beans than a virtual Bitcoin.

Of course the Dollar is going to crash, along with most other Western fiat, but the consequences of that crash are going to make it very difficult for Bitcoin to be a “store of value”.