I consider such an outcome to be highly improbable, as in the long history of hyperinflations (here is the Hanke-Krus table of 56 world hyperinflations [PDF] from 1795 through 2012 courtesy of Cato Institute, sorted by daily inflation rate at the peak), only rarely did the societal infrastructure collapse in the absence of a simultaneous war causing physical damage. Generally, people and businesses muddle through as best they can, exchanging depreciating paper for hard assets as quickly as possible. See Adam Fergusson’s When Money Dies for a realistic account of what it was like to live through the great Weimar inflation in the 1920s.

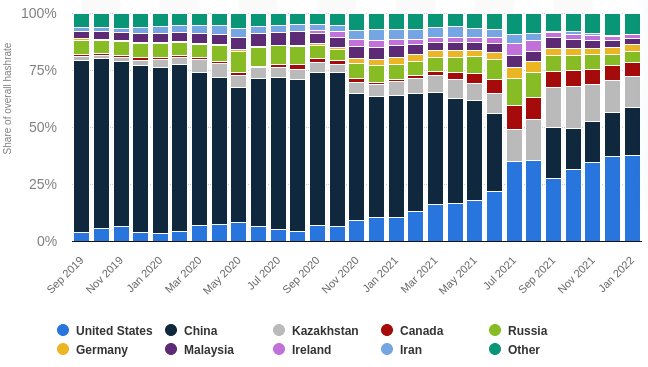

But even if the U.S. grid goes down, only about a third of bitcoin mining (transaction clearing) is in the U.S.

If that portion of the Bitcoin network goes down, transaction fees will increase, and miners in non-dollar regions will have an incentive to expand their operations. This will probably be accelerated by an increased demand for Bitcoin as a hedge against the depreciation of other fiat currencies and a means of clearing cross-border transactions.

Balaji moved from the U.S. to Singapore in 2020 (“get your ass and assets out while you still can”), so he would not be directly affected by events there.

That is a fair point about past experience. But muddling through was different in the days when people had local food, coal fires, and oil lamps. What is the potential for muddling through in modern economies so heavily dependent on reliable 24/7 electric power? Let’s hope we never find out.

One other thought on that – people have occasionally contrasted the social impacts of the Great Depression with more recent events. The Great Depression of the 1930s was truly horrible – genuine poverty, people reduced to eating cats & dogs. And yet, society was fairly orderly despite the stresses. Jump forward to the 1960s or to more recent events in West Coast cities – under much less desperate conditions, cities burned. It is a different world today from past episodes of hyperinflation.

Of the 56 episodes of hyperinflation listed in the Hanke-Krus table I cited in comment #41 above, 41 occurred since 1950, which excludes both those before widespread electrification and the effects of global war.

The decade with the most incidence of hyperinflation was the 1990s, primarily in ex-Soviet republics and former members of the Soviet bloc in Eastern Europe, which were hardly subsistence economies or pre-electrification. There may have been interruptions in utility service from time to time, but I am not aware of any of these countries descending into an apocalyptic widespread, long-term grid down societal collapse. The period of hyperinflation was generally rather short until it burns itself out, usually with the institution of a new currency. The wealth transfer from savers to debtors and the wiping out of pensioners and the wealth of the middle class is, however, permanent.

Some “swoop”—the last thing UBS, the largest Swiss bank with profits of US$ 7.6 billion in 2022, wants is to acquire much smaller Credit Suisse, which managed to lose US$ 7.9 billion that year, which is just about equal to their total profits over the previous decade.

What is going on and keeping the lights burning late tonight in Zürich is a shotgun wedding, with the Swiss National Bank (SNB—central bank of the Confederation) and Swiss financial regulator FINMA wielding the shotgun. Both are gripped by “fear of Monday”, since it appears SNB’s granting a CHF 50 billion credit line to Credit Suisse has done little or nothing to stop the tide of depositors wiring their money elsewhere, with the Financial TImes reporting outflows exceeding CHF 10 billion a day late last week. At that rate, the solvency of Credit Suisse is measured in days, if not hours.

UBS doesn’t want to do this deal, but when the central bank and regulatory agency decide to twist arms, they have ways to get the attention of even the largest banks. UBS is said to be holding out for a government guarantee against losses brought over from Credit Suisse of as much as CHF 6 billion. Credit Suisse’s retail banking business in Switzerland is profitable and sound (or at least it was until deposits started to bleed out last week), and a takeover by UBS would be a good deal for the latter, but the question is what happens to the other parts of Credit Suisse that have been generating the losses. Rumours are that a total merger of the banks may result in as many as 10,000 job losses.

We’ll see what they manage to cobble together before the opening bell on Monday.

Reportedly, the two largest shareholders in the now-defunct Credit Suisse Bank are Saudi National Commercial Bank (10%) and Qatar Investment Authority (7%) – both facing probable loss of their multi-million Swiss Franc investments.

First the Biden* Mal-Administration seized Russia’s investments in the US. Now Switzerland will likely stiff the cash-rich Arabs. It seems likely that the end result will be a flight of smart investors from North America & Europe. That could have consequences for the economies & people in the West

Update (10:30am ET[ 14:30 UTC]): So much for Credit Suisse thinking it has leverage by balking at the proposed CHF0.25 offer from UBS. Just hours after it was floated that UBS could buy Credit Suisse for $1BN, a proposal which the bank’s shareholders balked at, Bloomberg reported that authorities are now considering a full or partial nationalization of Credit Suisse - an outcome which would wipe out the equity and bail-in bondholders - as the only other viable option outside a UBS Group AG takeover. And yes, 0.25 is still more than 0.0.

According to BBG, “the country is considering either taking over the bank in full or holding a significant equity stake if a takeover by UBS Group AG falls apart because of the complexities in arranging the deal and the short time frame involved.”

Needless to say, the situation remains “very fluid” and is changing by the hour as authorities seek to finalize a solution for the bank by the time Asian markets open, which is late evening in Europe, the people said.

Earlier, Swissinfo reported, based upon the Financial Times:

Switzerland is preparing to use emergency measures to fast-track the takeover by UBS of Credit Suisse, according to three people familiar with the situation, as the banks and their regulators rush to seal a merger deal before markets open on Monday.

Under Swiss rules, UBS would typically have to give shareholders six weeks to consult on the acquisition, which would combine Switzerland’s two biggest lenders.

Three people briefed on the situation said UBS had indicated that emergency measures would be used so that it could skip the consultation period and pass the deal without a shareholder vote. The details are still being worked out, one of the people said.

Switzerland’s regulator Finma did not immediately respond to requests for comment. The Swiss central bank, Credit Suisse and UBS declined to comment.

The Swiss National Bank and regulator Finma have told international counterparts that they regard a deal with UBS as the only option to arrest a collapse in confidence in Credit Suisse and were working to reach regulatory agreement by Saturday night.

If the Credit Suisse shareholders have definitively rejected the UBS offer of CHF 0.25/share, the abyss has now opened up and nationalisation may be the only way to avert catastrophe as Asian markets are about to open.

Monday March 20 will be an “interesting” day. Several generations of multi-state profligacy - led by the good 'ole USofA - eventually comes due, as does use of the USD as the reserve currency. When the latter happens, ‘woke’ will devolve to a whole new meaning.

The Credit Suisse situation is being updated in real time by Swiss public broadcaster RTS, in French, at «Crise au Credit Suisse». The most recent report, updated at 16:08 UTC, says that the federal council (seven-member executive branch of the Confederation government) has been meeting since Sunday morning, and has announced an “important press conference” for Sunday evening, with the time not yet announced.

Bloomberg is updating the situation in frequent posts in English.

As regulators and bankers race toward a deal aimed at calming markets, officials are left grappling with brutal choices between trampling over shareholder rights or risking the escalation of the crisis. A low-priced deal with no say for owners risks lawsuits and hurdles to future international investors putting money into Switzerland. No resolution in the next 12 hours risks something even worse.

The deal is done. At 18:30 UTC, the Swiss Federal Council announced that UBS will acquire Credit Suisse, and that the Federal Council has, invoking its emergency powers under articles 184 and 185 of the Federal Constitution, which essentially allow it to rule by decree, bypassing the legislature, judiciary, and sovereign rights of the people to initiative and referendum for a “limited duration”, autorised the Swiss National Bank to provide liquidity assistance to Credit Suisse. In addition, UBS is granted a guarantee of CHF 9 billion against losses incurred in assets it acquires from Credit Suisse in the transaction. This money will be created out of thin air. The English version of the declaration is “Safeguarding financial market stability: Federal Council welcomes and supports UBS takeover of Credit Suisse”.

The terms of the deal are spelled out in press releases by the two banks (or, perhaps I should say, UBS and the smoking crater where Credit Suisse used to be).

Shareholders of Credit Suisse will receive one share of UBS for every 22.48 shares of Credit Suisse they now hold. This values Credit Suisse at CHF 3 billion, up from the first and second round offers of 1 and 2 billion by UBS. The equivalent Credit Suisse share price in the transaction is CHF 0.76/share, compared to CHF 2 at the close on Friday. Credit Suisse’s entire issuance of CHF 16 billion in AT1 Contingent Convertible bonds, representing the bulk of its capital, will be written down to zero, wiping out holders of these bonds. The bonds had already been written down to 35% of their original value as of the close of business on Friday.

The rule-by-decree order by the Federal Council overrode the legal and contractual obligations of both Credit Suisse and UBS to put the merger agreement to a vote of their shareholders. The consequences of this breathtaking departure from the rule of law, corporate governance, and shareholder rights for Switzerland’s reputation as a stable domicile for financial institutions have yet to be seen.

It will be interesting to see what happens to credit default swaps on the debt of UBS when European markets open tomorrow. I would not be surprised to see an emigration of wealthy clients from UBS to Swiss private banks which do not engage in the kinds of leveraged transactions that brought down Credit Suisse and in which UBS is a major player. UBS’s target Tier 1 capital ratio is 13%, which means, in a sense, their effective leverage versus coverage for unexpected losses is 7.7 to 1.

At time code 8:59 John Derbyshire (who actually worked in the area of financial risk management) points out that SVB was without a Chief Risk Officer for a substantial period of time during which SVB retained their well paid DIE officer.

Banks in Dubai have no restrictions on offering interest-bearing products. In fact, the UAE central bank has an official interest rate which follows that of the U.S. Federal Reserve because the UAE dirham (AED) is pegged to the U.S. dollar (AED 3.6725 = US$ 1). Devout Muslims who follow the Sharia prohibition on interest have access to a variety of Islamic banking financial products (deposit accounts, loans, insurance, mutual funds) which have been certified as Sharia-compliant. (For example, an Islamic finance bond may be structured as a profit-sharing vehicle which does not guarantee fixed income.) There is a good deal of cynicism about this. A banker in Dubai was quoted as saying,

We create the same type of products that we do for the conventional markets. We then phone up a Sharia scholar for a Fatwa … If he doesn’t give it to us, we phone up another scholar, offer him a sum of money for his services and ask him for a Fatwa. We do this until we get Sharia compliance. Then we are free to distribute the product as Islamic.

Although there are a few banks which offer Islamic products exclusively, most, including all of the Emirates branches of the big international banks, offer all of the same conventional products and services of any other money centre bank.

Of course not. Maybe I should have put in a smiley face.

Long time ago, when Islamic banking was newer, there was a really interesting article about a Western financial company consulting with Arabs while trying to find the guiderails for what was acceptable under Islamic guidelines. One of the analogs they used was someone lending a camel to his neighbor – Who got the camel’s milk? Who got the calf if the camel gave birth? Etc. Apparently they all had great fun with this.

The contagion of lawlessness at the highest levels spreads as fast as Covid. It makes the smash & grab retail thieves look like nothing, Back in the last memory-holed banking crisis, the Obama administration picked the winners and losers - “settled law” be damned. Union pension equity holders took a significantly smaller loss than bond holders, standing bedrock commercial law on its head. The law says bonds are superior to equity when it comes to bankruptcy. Not if TPTB say it ain’t so. So it was in the US, now, apparently, so it is in Switzerland. Such is the state of “first world” law. Next stop: Zimbabwe.

The Credit Suisse bonds which were written down to zero were what are referred to as “Additional Tier 1” (AT1) or “Contingent Convertibles” (CoCos), which totalled CHF 16 billion face value, now worth nothing. This is a debt instrument that was invented in the aftermath of the 2008 financial trainwreck, in which (terms vary depending upon the bond) the principal of the bond may be converted into equity in the issuer or written down if the issuer hits a trigger threshold indicating insolvency or capital falling below a prescribed level.

Because of the increased risk compared to senior debt, these bonds pay a higher rate of interest as a risk premium, and they are attractive to bond investors for that reason. (Banks do not usually hold AT1s of other banks because to prevent contagion they cannot include them in their capital as they do with other bonds.) The spread between senior debt and AT1s is considered a measure of the default risk of the issuer.

Now, before last Friday (2023-03-17), basically nobody imagined that AT1s would be written down to zero while paying off common shareholders first, albeit at a steep discount to the last quoted trade in the stock. Although the language of Credit Suisse and UBS AT1s apparently allow regulators discretion in writing down these bonds, everybody assumed that the centuries-old rule of debtors getting paid before common shareholders applied to them.

The total European market for AT1s is estimated at around US$ 175 billion, and holders of the bonds were stunned at the possibility they could be wiped out while shareholders received compensation. To avoid a rush to the exits, EU bank regulators and the Bank of England issued a statement on Monday 2023-03-20 which stated “Common equity instruments [stocks] are the first ones to absorb losses, and only after their full use would additional tier one be required to be written down. This approach has been consistently applied in past cases.” Or, in other words, “trust us—we won’t pull a trick like those perfidious buccaneers in Bern just did.”

This may not be a done deal. CNN reports that a law firm in Los Angeles was discussing litigation options with a group of Credit Suisse AT1 bondholders.

WisdomTree, an exchange traded fund listed on the London Stock Exchange that holds AT1s was down 7.4% in trading on Monday.

With the price of gold recently flirting with US$2000/troy ounce, I’ll bet some people will be discovering the “gold” they bought on eBay is actually tungsten (density 19.25 g/cm³) plated or clad with gold (density 19.3 g/cm³). I’m sure the scammers who sold it to them will say it’s just a “mix-up”.

Governments spent trillions to spur demandduring the pandemic by issuing debt that’s financed at very low interest rates…

The debt ended up held by banks, but due to supplyside inflationary effects of letting COVID run unmitigated and labor force shrinking, yet central banks keep raising interest rates

In turn, banks become unstable, due to all that underwater low interest state debt held by the banks…

So if governments need to bail them out, they might have to do so again by going into debt, which would restart the circle!